Many economists are predicting a global recession in 2023 with public and private finances under strain. Foreign investors are in the firing line, as governments under intense economic and political pressure, with high costs of borrowing and inflation, look to ‘big business’ to plug revenue gaps in their budgets. Aggressive tax policies and enforcement action may also result in more tax-related post-M&A disputes, as unwary buyers find themselves saddled with significant tax liabilities post-sale.

Over the next 12 to 24 months, we therefore expect to see an increase in high-value investor-State and commercial tax disputes – with a focus in particular on corporate income tax, windfall taxes, retroactive taxation, and novel taxes on the energy, telecoms and technology sectors.

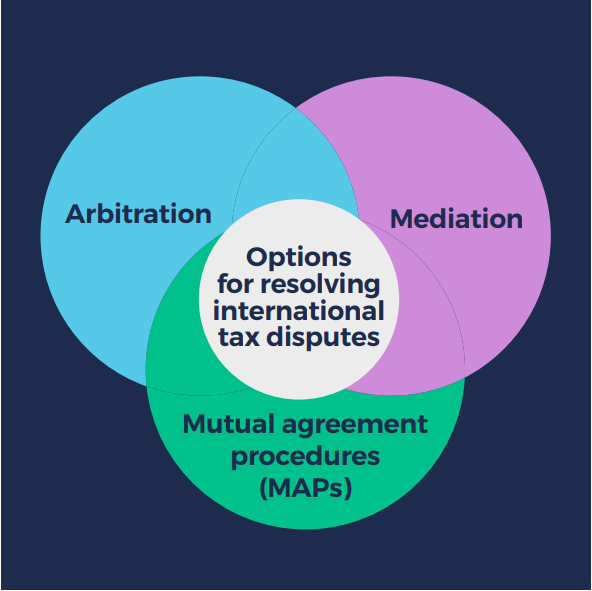

Alongside traditional domestic dispute resolution processes in the local tribunals and courts, contract and treaty-based arbitration – and other forms of alternative dispute resolution – will play an important role in ‘internationalising’ the large-scale tax disputes, enabling parties to find constructive and mutually beneficial solutions through an independent and neutral forum.

Options for dispute resolution – and the use of arbitration

It is, of course, natural for States to reconsider their tax policies in light of economic conditions, and that may involve recalibrating the State’s economic relationships with foreign investors. However, issues arise where States overstep the mark – for example, via unlawful tax assessments or rushed-through ‘windfall taxes’ that (at their most extreme) could amount to ‘resource nationalism’.

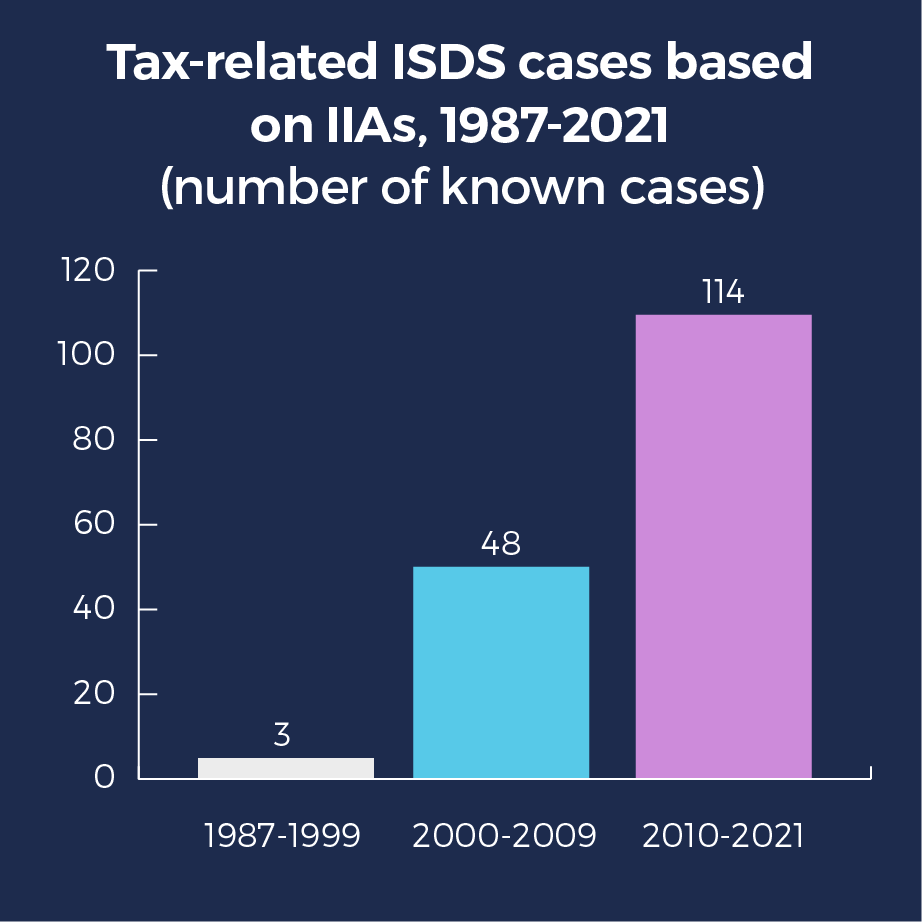

While the use of aggressive taxation against foreign investors is hardly new (indeed, we highlighted the increasing trend of ‘internationalised’ tax disputes in our 2018 Trends Report), what has changed over the past five years is that States and investors have become more sophisticated in their willingness to explore ‘internationalised’ options – such as arbitration – to resolve tax disputes. Similarly, alternative dispute resolution methods such as investor-State mediation and mutual agreement procedures (where a taxpayer’s ‘home’ State can engage with the taxing State via a formal treaty-based process) are on the rise, as investors and States look for alternative routes to constructive solutions.

Foreign investors in any jurisdiction will of course need to be strategic in deciding which cards to play and whether and how to submit to a local dispute resolution process. But by taking tax disputes – whether commercial or investor-State – out of highly charged domestic settings, the parties can work together to achieve a better understanding of the boundaries of lawful and unlawful taxation and best practices, with the benefit of specialist expertise from a ‘bespoke’ tribunal.

A clear illustration of the benefits of arbitration in a tax disputes context can be seen in India’s approach to a significant number of disputes with foreign investors arising out of a controversial 2012 retroactive tax law. That law (which retroactively levied capital gains tax on companies in an attempt to overturn Vodafone’s successful litigation in the Indian Supreme Court) came under scrutiny both within India and internationally. A combination of domestic litigation, investor-State arbitration and a highly structured dispute resolution process has allowed India and the relevant taxpayers to bring these disputes to an end, in turn buoying investor confidence in India.

Assessing the risks

As developments in the global economy take shape over the coming year, foreign investors should be (re)considering their tax risks and taking stock of their options for dispute resolution.

- For businesses maintaining operations in jurisdictions where the risk of aggressive taxation is likely to increase, the key is anticipation. It is often possible to predict which risks are most likely to arise – and what steps can be taken – having regard to sources of income and asset footprints, expert advice on recent trends in taxation, and the ‘bigger picture’ driving the political or tax authority agenda. Understanding and testing the local risks and knowing which advisers are available to help if the risk materialises is far better than having to react in a hurry.

- Similarly, new investors can anticipate their tax risks by reference to the very same factors – while also considering what types of tax protections are available to give all parties certainty as to their tax positions over the longer term (eg via an investor-State contract with provisions that ‘stabilise’ the applicable tax regime or applicable guarantees under bilateral or multilateral investment treaties). When structuring investments, it is also worth keeping in mind that certain types of investment treaties may only provide qualified protection in relation to tax measures or may exclude taxation measures from being subject to investor-State arbitration altogether.

- For investors who are looking to get out, divestments will give rise to their own tax issues, making the contractual allocation of tax risk with any potential buyer and the resolution of historic disputes even more important. Tax insurance may also be a useful tool in some cases, with insurers increasingly willing to insure certain types of high-value specific tax risks.